The first step to better household bill control starts with full tracking of expenses. Many people miss some costs when they plan for each month. The true total often sits higher than what first comes to mind. Your list should count both fixed and variable costs that change each month. Most homes have at least ten to twelve main bills to track. This full view helps spot where the most money flows out.

A good plan tracks each bill by size and when it comes due. The dates matter just as much as how much you must pay. Your paycheck dates should match when the big bills must be paid. This timing helps stop the cash flow crunch mid-month. Most banks now have apps that show all your costs in one spot. These tools make the task of bill tracking much easier.

Find Help When Bills Stack Too High

There are times when bills pile up past what your pay can cover. The choice then turns to which ones to pay now or put off. Your home and food costs must come first in these hard times. Most firms will work with you if you tell them you have cash woes. The talk may feel hard, but it helps more than just not paying. Your proof of why you face tough times helps them work with you.

Some people find that CCJ loans with no guarantor from a direct lender can help bridge gaps. These loans serve those with past court marks on their files. Your past should not block all paths to help in tough times. The firms that run these loans know how to check if you can pay. Most look at what you earn now, not just your past woes. This choice helps when bills must be paid to keep your home life safe.

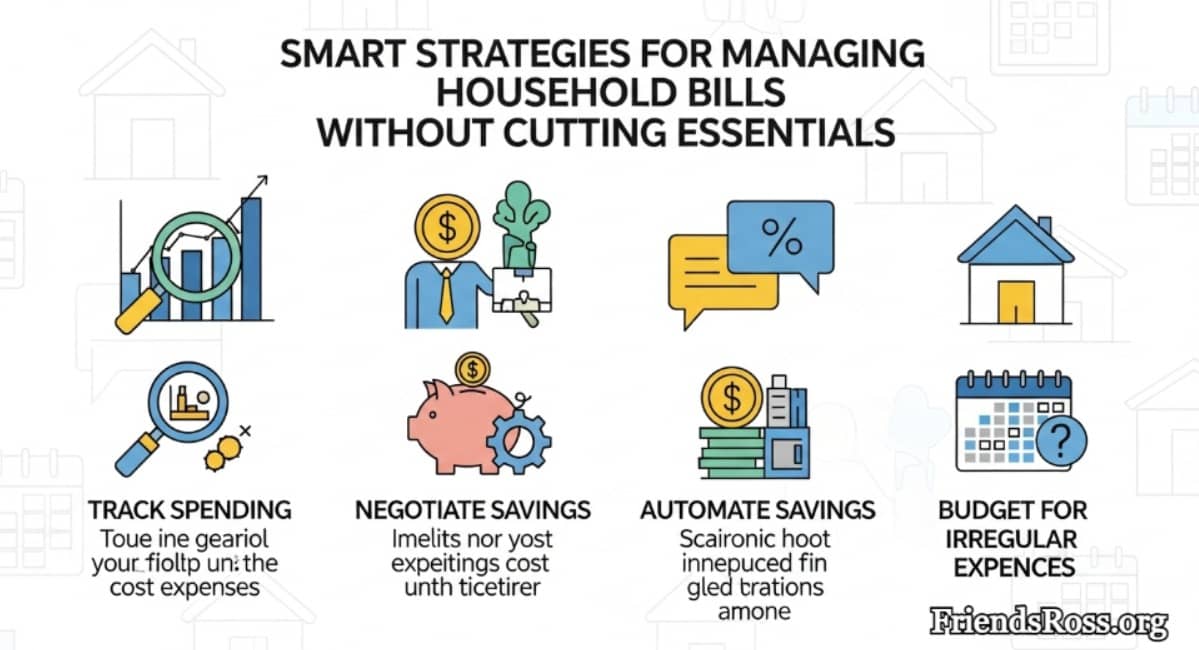

Track Your Bills

Listing all monthly bills reveals the true cost of living. Most people get surprised by how much they actually spend. Seeing everything in one spot shows where the money goes. This simple step identifies which costs keep rising too fast. People often find expenses they had completely forgotten about.

Fixed costs stay the same while other bills change each month. Rent never changes, but power and food costs always vary. Knowing this difference helps focus on bills that can change. Smart people track both types to manage their money better. This knowledge helps make tough choices when funds run tight.

- List every monthly bill on one simple sheet

- Check which months certain bills hit their peak

- Review three months of statements for hidden costs

- Set calendar alerts for when each bill comes due

Haggle for Better Deals

Service companies raise rates while offering deals to new customers. Most firms will lower your bill if you ask. A quick phone call often saves hundreds over the year. Companies count on people being too busy to notice increases.

Do research before calling to find what competitors charge. Mention these better rates during your call for leverage. Start with non-essential services that you could cancel. These companies usually have more room to offer discounts. Many firms have special rates they never advertise to customers.

- Ask directly for the customer retention department

- Question any service features you rarely use

- Compare rates with at least two competitor offerings

- Prepare to switch if they refuse better terms

Cut Power Costs

Power companies often charge less during off-peak evening hours. Running appliances during these times cuts costs considerably.

Simple home fixes save money without reducing comfort levels. Draft stoppers for doors keep heat from escaping rooms. Many appliances use power even when nobody turns them on.

- Find cheaper off-peak hours from your power company

- Run washers and dryers during discount time periods

- Check other power companies for potentially better rates

Change Payment Timing

Bills that arrive clubbed together create unnecessary financial strain. Most companies allow customers to change their monthly due dates. This simple change helps match bill timing with payday.

Breaking these costs into monthly payments eases budget pressure. Many insurance companies offer this option without extra fees. This approach prevents the stress of large lump sum payments.

- Request due dates that fall shortly after payday

- Create a calendar showing when each bill arrives

- Group similar bills together for easier tracking

- Focus first on adjusting dates for your biggest expenses

Use Bonus Money

Extra income provides opportunities to manage rising household costs. Tax refunds and work bonuses should help with bills. Using unexpected money wisely brings lasting financial benefits. Setting aside half for necessary expenses makes sense.

Side income can offset specific bill increases very effectively. Seasonal work helps during months when certain bills peak. Selling unused household items generates cash for rising costs. Having particular targets for extra money prevents wasteful spending. This approach turns occasional windfalls into practical financial tools.

- Choose which bills would benefit most from extra funds

- Apply at least half toward essential household expenses

- Find temporary work during high-bill seasons

- Plan for using tax refunds wisely

Use Extra Cash Wisely

Bonus cash helps pay bills when regular income falls short. Tax refunds and work bonuses arrive several times each year. Many spend this money on fun purchases or wishes. Smart planning directs these funds toward pressing household bills instead. This strategy keeps monthly budgets from getting overwhelmed by costs. Bills keep rising while regular income often stays the same.

Side jobs bring in money that can offset increasing bills. Selling unused items adds extra funds for household expenses. Plans for this money should exist before it arrives. Assign each extra dollar to a specific bill beforehand. This prevents funds from vanishing on less important purchases. Many bills become manageable with just a little extra help.

- Use half of any bonus money for pressing bills

- Keep a list of which bills need extra help

- Put bonus cash in a separate dedicated account

- Look for seasonal work when certain bills increase

- Sell items around the house that nobody uses

- Save tax refunds specifically for annual expenses

Conclusion

Small steps add up when spread through all your home bills. Your phone plans might have bells you pay for but do not use. The banks may charge fees for things you could get for free. Most firms hope you will not check what they bill you each month. The task of bill checks takes time, but pays you back much more. Just one hour each month can save you tens or more on bills.